A POCKET GUIDE TO ACTIVIST INVESTORS

THE MARKET`s ultimate POWER PLAYERS

Who Are They? What Are Their Goals? Why They Can Impact Portfolio Decisions.

My dear Friends,

You probably associate “activism” with climate marches, social campaigns, protest marches, or people with a mission to improve society, environment, and all the other things that need improving, while the rest of us keep doing what we always do.

In finance, however, activism is nothing benevolent but wears a sharper suit.

There is a particular breed of investors who do not simply buy shares, sit quietly, and hope the company will make a profit. Activist investors arrive with a judgment, ultimata, strategies, and, quite often, enough money to make a boardroom apprehensive.

After a quieter spell during the COVID-19 pandemic, activist investors are back in full force: well-funded, highly focused, and ready to shake up companies in pursuit of greater value. They are not a passing market mood. They are here to stay.

So, I have put together this easy-read pocket guide for you: a no-nonsense, no-financial-market-lingo introduction to the market’s power players, their true intentions, how they operate, and why their moves can matter to your portfolio.

So, be curious and ready to learn more about the mystery surrounding activist investors.

The Investors That Make Everybody Nervous

As you will see, the pocket guide reveals that activist investors are neither out to improve society, nor to save the planet, nor to fight for equal rights for minorities; they are a type of shareholder who buys shares of a company only to pursue personal goals. namely to make huge profits. The activist investor is not a silent and passive investor but, as the term suggests, a very active shareholder not only with a plan but a strategy.

Activist investors first strive to take a big stake in a publicly traded company and then push for change. Not quietly. Not vaguely. Often, by putting pressure on the board, rallying other shareholders, and generally causing enough disruption to get the company management super nervous. Either directly appealing to or putting heavy pressure on the company’s board of directors or overriding the normal advisory process.

The idea is usually simple: they believe the company is undervalued, underperforming, badly managed, or simply not making enough money fast enough. Traditional value investors may wait patiently for the market to recognise a company’s true worth. Activist investors want change sooner, have a very specific plan, and will implement it, if needed, by any means necessary..

They may talk about improving the company, unlocking value, or protecting shareholders. Sometimes they may even be right. But at the end of the day, activist investors are primarily looking after their own interests, which is worth remembering. They are not some kind of good Samaritans for financial markets; they are primarily looking out for their own best interests.

A Who´s Who Of Activist Investors

Activist investors do not all arrive with the same agenda, temperament, or appetite for disruption. Some come armed with spreadsheets. Some come with governance complaints. Some have their very own idea about who should be running the company.

The most feared are hedge fund activist investors; they are by far the most aggressive kind. They are super-focused, with lots of money, a player who buys a meaningful stake in a public company and starts pushing for visible change. That change could mean a new strategy, a sharper financial structure, a different management team, or fresh faces on the board. Subtlety is not always the chosen accessory.

Then there is the governance-focused activist investor. This type is less interested in creating upheaval and more interested in how the company is actually run. They may question executive pay, board independence, audit quality, risk management, or whether leadership is serving shareholders properly. Not glamorous, perhaps, but governance is where many expensive mistakes begin.

Another type is the strategic activist investor. This one looks at the company and asks whether it has become too multidimensional, has no strategy, or is too attached to branches it should probably have let go of years ago. They may push for mergers, break-ups, spin-offs, or a return to the core business to increase revenue.

There are also operational activists. They look closely at how a company operates day-to-day and argue for better margins, leaner structures, cost discipline, or improved efficiency. This is not the most romantic corner of investing, but neither is watching a company waste money with great confidence.

More recently, activist investors have also become louder around capital allocation. That simply means how a company uses its money. Should it reinvest in the business, buy back shares, pay dividends, sell assets, reduce debt, or stop funding projects that seem to exist mainly because someone once made a persuasive presentation? These questions can matter enormously to shareholders.

And then there are the activists who focus on management and leadership. They may argue that the current team is not delivering, that the board is too passive, or that the company needs new people in charge. This is where activist investing can become especially uncomfortable, because jobs are at stake, and some might lose their key cards in the process.

This pocket guide is not intended to turn you into an activist investor, but to familiarise you with the different types, help you understand what they are pushing for, and show why their moves can matter when your portfolio is exposed to the companies they target.

The Activist´s Strategy

Activist investors are rather good at spotting what they believe a company has failed to see, fix, or use properly: weak management, lazy strategy, bloated costs, neglected assets, or a business that could be worth more if someone finally stopped lamenting but started dealing with the problem.

They spot that gap, and usually arrive with a plan. Not always a gentle one. Their aim is to push the company into action and, ideally, increase shareholder value along the way. Their proposals tend to fall into a few familiar categories:

- Improve the business. They may push for cost reductions, higher revenues, better margins, or a sharper operating strategy. In less polished terms: stop wasting money and start making more of it.

- Sell, split, or simplify. An activist investor may argue that a company should sell an underperforming division, separate into different business units, or focus again on what it actually does best. Large companies have a special talent for becoming complicated and then calling it “strategy”.

- Change how the money is used. Activist investors may pressure a company to repurchase shares, reduce debt, pay dividends, sell assets, or restructure its capital. This is where the question becomes: is the company using its money wisely, or merely keeping it busy?

- Shake and wake up the board. They may demand changes to the size, composition, or independence of the board of directors. Sometimes this means asking whether the people overseeing the company are truly challenging management, or just nodding at the status quo.

- Run a campaign. Activist investors often build public or private campaigns to win support from other shareholders, analysts, and sometimes the media. These campaigns can move quickly, especially when the activist has enough capital, confidence, and vigour to make the company listen.

- Push for faster results. An activist investor may believe the company is underperforming, moving too slowly, wasting assets, tolerating weak management, or failing to use its money properly. They push for quicker changes because they think the company’s value is trapped by poor decisions or inertia. However, pursuing short-term gains at the expense of sustainability. As an investor, you need to understand that activist investors’ view is short-term: to realise substantial profits on their investments in a short period and move on. A long-term approach, slow growth or sustainability of a company is not on an activist investor’s mind.

Boom Of A Boardroom Defence Industry

Many companies see activist investors less as helpful shareholders and more as hostile attackers. Not because the activists arrive with torches and medieval helmets, tempting though the image may be, but because their arrival usually means uncomfortable and aggressive questions are coming, often with layoffs to follow.

They may challenge the company’s strategy, criticise management, demand board changes, question executive pay, push for asset sales, or argue that the business is not using its capital well enough. For a board and management team used to setting the agenda, this can feel less like constructive dialogue and more like someone walking into the room, taking the pen, and rewriting the plan. Thus, they feel threatened, and if they have compassion, they fear for their staff as well.

Sucess, and timeline of activist investor campaigns

The advisory industry was quick to sniff out an opportunity. Consulting firms, law firms, investor-relations specialists, and governance advisers now help companies prepare to fend off activist campaigns. There is serious money in telling nervous boards how not to become the next target. Consultants, whatever the type, have found a way to cash in on the “hostile attacker” contagion.

It is common-sense advice: build a response team, strengthen shareholder relationships, review the business portfolio regularly, check whether the strategy still makes sense, address ESG concerns before they become easy targets, and ensure governance and executive compensation can withstand scrutiny. In other words, fix the obvious weak spots before someone with capital, the necessary vigour, and a press assault points them out.

If an activist campaign does arrive, the defence intensifies. Advisers may help create response teams, prepare board talking points, brief management, manage media pressure, communicate with shareholders, and build arguments against the activist’s demands. None of this comes cheaply. Defending the boardroom has become a business in itself, and a very lucrative one.

The activist investor may be chasing value, but the rather new “hostile attacker defence industry” has quickly found its own very profitable niche of the dilema.

Why Activists See What Others Miss

Activist investors usually arrive with more than money and an opinion. They often have outstanding analytical skills, deep business experience, and teams who know how to take a company apart on paper before anyone has even booked the first tense meeting.

This is one of their biggest advantages. A normal investor may look at the share price, the dividend, the brand name, or the general mood around a company. An activist investor goes much further. They study the balance sheet, margins, debt levels, capital allocation, management decisions, board structure, competitors, hidden assets, underperforming divisions, and all the places where value may be sitting quietly, uninvited and underused.

That analytical work matters because activist investors are not simply saying, “We think this company could do better.” They usually arrive with a specific argument. They may claim the company is spending too much, growing too slowly, holding on to the wrong assets, rewarding management too generously, or allowing a weak strategy to drag down the share price. In finance, a strong opinion is nice. A strong opinion backed by numbers is hard to ignore.

Their business expertise is another super valuable perk. Many activist investors understand how companies are built, financed, managed, restructured, sold, split, or turned around. That means their recommendations can be very precise. They may push for a new strategy, cost reductions, asset sales, debt restructuring, share buybacks, or changes in how the company uses its capital.

They may also move directly into boardroom territory. An activist investor might demand a seat on the board, call for the appointment of independent directors, or target specific directors for removal. This is where the exercise stops being a polite investment suggestion and becomes a very real challenge to the people running the company.

This is the reason I wrote this pocket guide. Because the above-mentioned may impact your portfolio, should you hold shares in a company under “attack”? There is something important you should bear in mind as an investor: activist investors often see possibilities that ordinary shareholders may not have the time, access, or expertise to spot. That does not make them automatically right, noble, or charming. But it does explain why companies take them seriously; their campaigns move share prices, influence board decisions, and shape a business’s future direction.

Take-Away

Activist investing is a form of value investing, albeit an aggressive one

Activist investors look for weaknesses, flaws, or unresolved problems that may cause publicly traded companies to be undervalued

Their goal is to improve the company’s performance, realise the value they pushed for, and then exit, usually with a sizeable profit

They buy enough shares in the target company to gain voting power and make themselves difficult for the board to ignore

The activist investor instigates strategic initiatives, such as restructuring the company, and, if necessary, implements them by force, often by using unsavoury methods

The new-generation activist investor is more focused on implementing ESG regulations, still aiming to maximise their profit

The activist´s methods, however, rarely align with ESG regulation

The activist investor´s investment horizon is very different from that of the average investor. The first operates with a short-term view. The latter is focused on the long-term outcome of an investment

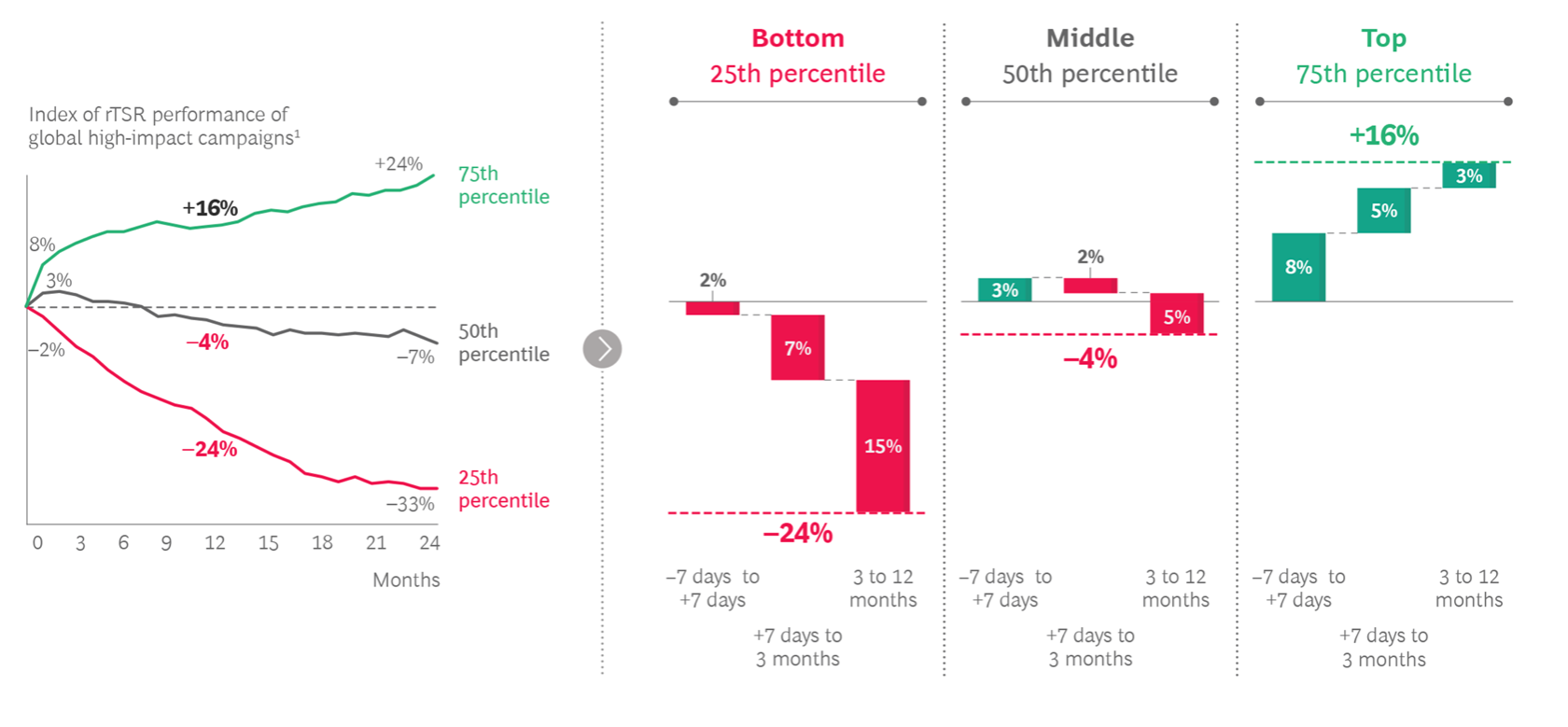

Companies can lose between 4% and 25% of Total Shareholder Return (TSR), a decrease in return per share, within a year of an activist attack.

Contrary to widespread belief, activist investors are no more clever than others. They sometimes lose money too.

Four out of every ten campaigns over the past five years occurred outside the US, with the biggest surges in Europe and Asia

The Activist Investor´s Pocket Guide

Now, you can see that activist investors rarely appear by accident. Their campaigns usually follow a fairly recognisable pattern. Not every case unfolds in exactly the same way, but the activist’s playbook tends to follow a recognisable pattern.

- Build a position. Start by buying a meaningful number of shares in the target company, do this in a relatively short period of time. For better financial exposure, a louder voice. In the shareholder world, ownership is influence.

- Make your case. As soon as you have a stake, begin to engage with the company’s board and management. Argue for the changes you believe will increase value, whether that means a new strategy, asset sales, cost reductions, board changes, or a different use of capital.

- Go public. If private conversations stall or do not move quickly enough, go publicargument public. Use letters, presentations, interviews, media coverage, investor calls, and public campaigns to explain your position and attract support from other shareholders.

- Build pressure. Publicity matters because it changes the balance of power. The more shareholders, analysts, and commentators pay attention, the harder it becomes for the company to ignore you quietly. Even if the board resists, the conversation has already moved beyond the boardroom.

- They may force a fight. If negotiations stall, the dispute can escalate into a proxy fight, try to win shareholder support to replace directors or gain control over parts of the board. Stop having polite disagreements; go for a full-on boardroom contest.

- Push Changes. Gain enough influence to make sure your changes are carried out. That could mean a new board composition, a new strategy, a restructuring, a divestment, or a sharper focus on shareholder returns.

- Exit when the job is done. Once the objectives are achieved, sell your shares and move on. Do not be a sentimental owner. You came for value, pushed for change, and once the value has been realised, the next opportunity begins to look far more exciting.

The pocket guide helps you to understand that activist investors are not passive passengers in the market. They are active, demanding, and often disruptive players who can change a company’s direction. Whether you admire them, dislike them, or simply want to understand them, knowing how they operate helps you ask the right question if one of your assets is under “hostile attack.”

” Activist Campaigns are all too likely to destroy value, so it is essential that companies preempt them.”

Boston Consulting Group

The New Set Of Activist Investors

A newer generation of activist investors has entered the scene, and they claim their campaigns do not follow the old “buy shares, demand change, make money, leave” routine.

Yes, returns still matter. Finance has not suddenly discovered selflessness. Some activists now combine financial demands with pressure around climate risk, employee issues, governance, board quality, executive pay, and how responsibly a company is being run.

Their argument is simple: these are not just “soft” issues. Poor governance, weak leadership, climate exposure, or badly managed social risks can damage reputation, performance, investor confidence, and ultimately the company’s value.

Some activists now arrive with both financial and ESG arguments. Others may attack from different sides at once: one pushing for stronger returns, another for environmental or governance change. For the company, that can feel like being squeezed from several directions at once.

The old “greenmail” campaigns were mostly about financial pressure. Today’s activism can still be hard-nosed, but the agenda has widened. It is now about money, risk, reputation, responsibility, and whether leadership is fit for the future.

A softer playbook, really?

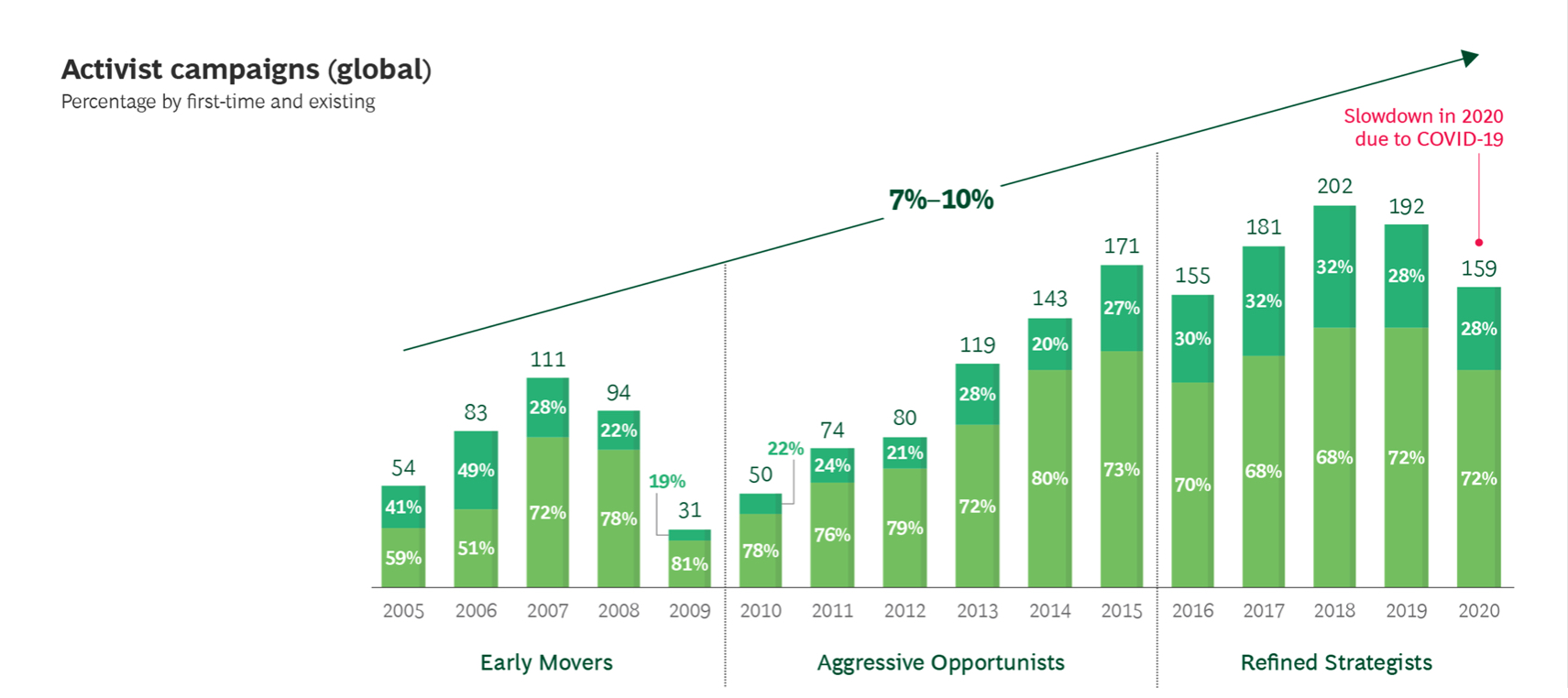

According to a Boston Consulting Group study, activist investing has changed quite a bit. In the past, many campaigns were mainly about short-term financial engineering: push hard, extract value, move on.

Today, the picture is more layered. Activist investors are increasingly arguing for changes that put companies on a stronger long-term footing. Between 2016 and 2020, more than half of all campaigns worldwide were driven by governance and strategic issues, not just quick financial fixes.

ESG has also become a much bigger part of the story. Climate, diversity, and related demands accounted for nearly 20% of activist interventions over the last five years. Assets behind ESG-driven campaigns have grown from about $20 billion to more than $90 billion, and these campaigns have reportedly become three times more successful over that period.

So yes, activist investing has become more modern, more strategic, and, dare one say it, slightly more avant-garde. Still, let’s not get carried away. Maybe the language has changed, but the goal is still the same: maximum disruption in a short period of time, a fast company turnaround, and an even faster exit to maximise profit. Activist investors, including the modern type, are still considered an “attack” on any company.

The prevention of, or response to, an activist attack ” is an art, not a science.”

(Harvard Law School).

Inside The New Playbook

- Aggressively criticise a company’s governance, management, business, strategy, sustainability and ESG strategies. Go public if necessary.

- Present a “white paper”, public documents or statements of your strategy, goal and timeline, for management, staff, business practices, and improvement or implementation of ESG standards.

- Coax and rally institutional investors and research analysts to support your arguments and strategy for chance

- Use stock loans, options, derivatives and other devices to accumulate positions secretly, announce surprisingly large, leveraged economic stakes, or increase voting power beyond the economic equity of your investment.

- Invest in thorough due diligence and third-party consulting services to analyse the target’s business strategy, operating margins, and/or ESG impact.

- Lure the company’s retail shareholders, through internet forums and social media channels, weekly mailings, telephonic outreach, local newspaper advertisements and user-friendly infographics. No method is off limits.

- Blackmail with repeated campaigns at the same company, regardless of the outcome of the initial campaign, or joining with other activists to converge on the same company at the same time

Let’s be honest, these new methods are neither new nor do they align with ESG standards. Honestly, none of the above can be considered good governance.

The Increase In Gobal Activism

Activist investing is no longer mainly an American story. Over the past five years, four out of every ten activist campaigns took place outside the US, with the strongest growth in Europe and Asia. Between 2016 and 2020, activism in those regions grew sharply, while activity in the US rose much more slowly.

That matters because activist investors do not behave in exactly the same way everywhere. Many campaigns still have a local character, shaped by the region’s business culture, shareholder rules, and appetite for public confrontation. In Asia, for example, activists are often more focused on balance sheet opportunities, while public criticism tends to be less common. Influence is still often applied behind closed doors, because not every market enjoys a public boardroom quarrel quite as much as the West seems to.

Still, activism in Asia has grown dramatically. There were 106 activist campaigns in Asia last year, compared with 94 the year before and only 10 in 2011. That is quite a shift for a region long considered less suited to public shareholder activism.

The broader pattern is clear: activist campaigns are becoming more global, institutional investors are becoming more vocal, and companies can no longer assume they are immune simply because they are large, respected, or doing reasonably well. Most targeted companies have underperformed the market, but not all. Some companies with strong shareholder returns have also found themselves under pressure.

“In Asia, as regulators look to protect the interests of minority shareholders, corporate governance has risen up the agenda … activist investors now have more power to push for change in the companies in which they have invested,”

David Hunker, JP Morgan

Activist investors also watched closely during the pandemic, not only to see how companies protected their finances, but also how they treated employees, customers, and wider stakeholders under stress. That gave activists another way to question whether leadership was truly managing the business well.

All companies are vulnerable. Although most companies targeted underperformed the market, a fifth, however, had strong shareholder returns. Management can quickly lose control of the narrative, with the TSR (Total Shareholder Return) trajectory nose-diving, typically in the first three months after the attack.

It should be noted that activist investors can raise valid concerns and can push companies towards better decisions. Others may create disruption that destroys value rather than builds it. For companies, the lesson is simple: do not wait for an activist to arrive before overdue change is implemented. For investors, the lesson is just as useful: when activism appears, look beyond the noise and ask what weakness, opportunity, or unresolved issue has drawn it in.

Activist Investors Vs. Real Value, The Truth

So, do these power players bring real value? Sometimes, yes. An activist investor can expose a weak strategy, sloppy governance, poor use of capital, or management decisions that should have been questioned long before anyone launched a campaign and a press release.

But let’s not mistake activist investors for generous market Samaritans or a breed of investment geniuses. They may speak about value creation and shareholder rights, and sometimes they are absolutely right. Still, at the end of the day, they are mainly looking after their own interests. Useful to remember before we cast anyone as the heroic rescuer of underperforming companies.

“It will allow them to say that they are putting voting power back into the hands of the beneficial asset owners and also deflect some of the criticism that BlackRock has received,”

Douglas Chia, Soundboard Governance

They can also be wrong. Their timing may be poor, their ideas may take years to work, and they can lose money like everyone else, though often with a better legal team and more patience. Smaller investors should be careful about copying an activist investor’s buying or selling strategy simply because it looks clever from the outside. Unlike the average retail investor, they not only have a backup team of analysts and plenty of cash to fall back on, but enough sang froid and drive to press their strategy against all odds.

While some shareholder campaigns force bold changes that deliver positive near-term results, these are the minority. Most companies lose between 4% and 25% of total shareholder return (TSR) within a year of an activist attack. Senior leaders are also more likely to lose their jobs; data indicate that activism nearly doubles the possibility of CEO turnover.

The risk for retail investors is simple: activists purchase large blocks of stock, usually without getting noticed, and they offload their shares rather quickly, usually in substantial amounts, once their objectives are achieved. As a result, the share price will drop significantly, leaving retail investors unprepared and facing losses.

It is important to note that activists have a very different investment horizon from the average investor. And, they are far more willing and able to accept a loss on their bets.

Are activist investors a role model for smart investing? Are their strategies worth copying? This decision will depend very much on your mindset, especially your risk tolerance and how disruptive you can be. But remember their investment horizon, risk appetite, and ability to absorb losses are very different from yours.

The point of this pocket guide is not to admire or condemn activist investors. It is to understand them. They can create value, destroy value, reveal value, or simply create a spectacular amount of noise around value. The pocket guide gives you enough knowledge of how they operate, so you are no longer just watching the drama. You can now read the signals and can act accordingly if necessary.

THE VERDICT: Know Your Investments. Stay InforMed. Act In Time

Activist investors can bring real value, but they can also be very destructive.

Contrary to the rumour, they are not the superior investors! Neither are they good Samaritans on a mission to save companies. They do it to make a substantial profit.

Once they have achieved their objective, they quickly offload the company´s shares. This often happens to the detriment of small investors, who incur losses as the market is flooded with the company’s shares and the share price declines.

An insight worth knowing:

Work your wealth to have choices for life!

– Yours Harper