Welcome back,

The US Debt Ceiling Crisis

-The impact on global investing-

My dear Friends,

Not to worry, I will not be alarmist, but honestly, the stakes are pretty high right now.

It seems-as so often in the past- the US has again reached its debt ceiling. It seems the US will be out of money by June 1st – as so often.

So far, the US has reached its debt ceiling 78 times and always accompanied by panic-mongering. Yet, previous debt ceiling crises were resolved at the 11th hour, and life went on as before.

The big question is, can the debt crisis be solved despite the differences between Congress and the government? Far more important, what will happen to the global economy and global investors should no solution be found?

Hang in there for a few minutes because this is important for global investors!

The origins

Let’s take a look at what the debt ceiling is all about. The Department of the Treasury says:

The debt limit is the total amount of money that the United States government is authorized to borrow to meet its existing legal obligations, including Social Security and Medicare benefits, military salaries, interest on the national debt, tax refunds, and other payments. The debt limit does not authorize new spending commitments. It simply allows the government to finance existing legal obligations that Congresses and presidents of both parties have made in the past.”

If the US government hits the debt ceiling and exhausts all other options, it can no longer borrow. Meaning it will run out of money soon after it hits the limit and temporarily default on obligations.

If the Treasury Department is not able to borrow additional money, the United States could default on outstanding loans. Credit rating groups may downgrade U.S. credit ratings as a consequence. Additionally, a default would negatively impact the U.S. economy and international financial markets.

The early days

The debt ceiling was introduced at a time when the US Congress was much more involved in borrowing money. Each time treasury needed money, they had to ask Congress to authorize the payment for whatever was due.

Congress had to authorize the Treasury to issue bonds to pay for certain projects. Like the Panama Canal, for example. In 1902 the US Government authorized the US Treasury to issue bonds to pay for the construction of the canal-the Panama Canal Act.

Other projects were funded with their own bond issuances or their own taxes. The Treasury had to keep those piles of money separated.

The turning point came in 1917 when the U.S. entered World War I financial needs skyrocketed. Treasury had to ask Congress for permission each time they needed money to pay for the war effort. That was highly impractical.

So Congress did away with the rather tiresome procedure. Under the Second Liberty Bond Act, the government allowed the Treasury to issue bonds without having to ask for authorization. The catch, a certain limit was given in order not to lose control. This, over time, evolved into the debt ceiling the US has now.

The Treasury has the flexibility to decide the timing and the structure of different debt issues. The amount of the debt, however, is determined by the deficit in the federal budget. This is, in turn, controlled by Congress.

The debt ceiling or debt limit is the cap on how much the Treasury can borrow to pay for everything.

The idea was to give politicians a pause to think about how they’re spending money. That is a nice thought. The question is, was it effective?

“I do think it is generally understood that, you know, the consequences of bumping up against the ceiling and then potentially defaulting on some debt as it becomes impossible to borrow would be very bad for the economy,”

Eric Hilt, Professor for Economic History, Wellesley College

The many changes

The first overall debt limit was established in 1939. Since then, the U.S. economy, and the national debt, have grown significantly.

Over the past seven decades, the debt ceiling has been raised a whopping 78 times. In 2011, the delay in agreeing to a new limit resulted in the US losing its coveted AAA credit rating. Consequently, borrowing costs rose significantly.

In 1940, Franklin D. Roosevelt was president, and the debt ceiling was $49 billion, which amounted to 48,32% of GDP. By 1945 the debt ceiling was at $300 billion, the equivalent of 134,53% of GDP. The national debt has increased under every presidential administration since Herbert Hoover. However, between the 1950ies and 2008, the debt ceiling never exceeded 78% of GDP. In Total, the United States has raised its debt ceiling at least 90 times in the 20th century. It should be mentioned it has never been reduced.

Heading for the ceiling

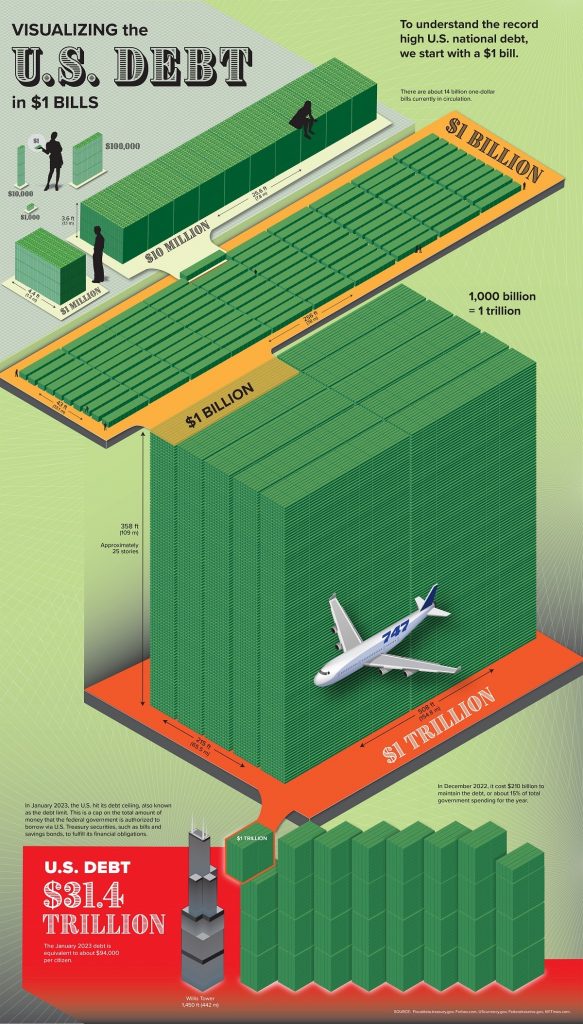

US Congress has authorized trillions of dollars in spending over the last decade. So, the United States’ debt has nearly tripled since 2009. By April 2023, the debt had reached $31.4 Trillion, or 126,43 % of GDP.

In comparison, the EU’s debt is 91,6% of GDP, the UAE’s 38,3, and Australia’s 35,8%. Japan is the only country exceeding the US. With 237% of GDP, Japan has the highest debt-to-GDP ratio in the world. Japan, however, never defaulted.

Clearly, the US government spends more than it takes in through revenues. A debt default would force it to stop paying out. Quickly military salaries, government retirement payments and other benefits would dry up. And if the US can’t pay interest on its debts, the rates it pays to borrow money will rise.

However, one question arises: do other countries have a fixed debt ceiling too?

Few countries set formal limits on public borrowing because they end up being tools of political blackmail. This, however, does not mean other countries can borrow without limits. Unlike the US, most countries that have a debt limit to encourage fiscal restraint tend to structure them as a percentage of GDP instead of choosing a nominal value.

The only other country in the world which has a debt ceiling similar to the United States is Denmark. Yet only the US is regularly pushed to the edge of an economic crisis. Denmark has set the ceiling intentionally high enough to avoid political bickering.

Australia, on the other hand, did introduce a debt limit in 2008. The idea was to bolster fiscal credentials, but Australia ditched the debt ceiling in 2013. It had become a source of constant political bickering.

When the clock ticks

Raising or suspending the debt ceiling becomes necessary when the government needs to borrow money to pay its debts. For much of the past century, raising the ceiling has been a relatively routine procedure for Congress.

The US Congress can also choose to suspend the debt ceiling or temporarily allow the Treasury to supersede the debt limit.

Since 2013 the debt limit has been suspended seven times.

Since 2011, a new style of debt limit debates has become a highly charged political football. In 2011, heated discussions between Democrats and Republicans caused a lengthy deadlock. Eventually, the debt ceiling was raised only two days before the Treasury ran out of money.

However, the brinkmanship triggered the most volatile week for the global stock markets. Worse, the US credit rating was downgraded for the first and only time ever. The delay in reaching a deal did increase US borrowing costs by $ 1.3 billion for 2011 alone.

In 2013, when the debt ceiling was set to expire again, the neverending haggling forced the government into a shutdown. The same happened in 2021, and the country inched close to economic peril. In the end, Democrats raised the debt ceiling without the vote of the Republicans. Luckily Democrats had the majority in Congress.

The ripples, however, were felt around the globe, and stock markets were extremely volatile.

Yet now, for the first time in history, economists contemplate the unthinkable- a US default.

Big stakes ahead

If the Treasury Secretary is correct, there are just a few precious weeks remaining for Congress and the White House to reach a debt-limit accord. Or else this might end in “an economic and financial catastrophe.”

The fact is without a sustainable compromise, US finance will fall off the cliff by June 1st.

Sadly this time, the differences between Congress and the US administration seem to be unbreachable. Republicans want spending cuts tied to lifting the debt limit. Democrats insist on a “clean” bill with budget discussions to follow. The chances for a quick fix are very low.

However, let’s bear in mind that neither side can have any interest in the US defaulting on its debt.

Wacky 11th-hour solutions

Some “experts” have come up with alternative solutions.

“Failure to meet the government’s obligations would cause irreparable harm to the U.S. economy, the livelihoods of all Americans and global financial stability,”

Janet Yellen, Treasury Secretarysince 2021; former Federal Reserve Chairwoman

The potential repercussions

The failure to find a solution would result in a downgrade by credit rating agencies. Thus increasing borrowing costs for businesses and homeowners alike. Consumer confidence would drop, and that could shock the financial markets and tip the global economy into recession. Goldman Sachs economists have estimated that a breach of the debt ceiling would immediately halt about one-tenth of U.S. economic activity.

According to centre-left think tank Third Way, a breach that leads to default could cause the loss of three million jobs in the US. Mortgages would spike. Rising interest rates would increase the US national debt by $850 billion.

Even a prolonged standoff could result in something a lot worse than what happened in 2011 or 2013. Why? Short-term loans are often backed-up with US Treasuries as collateral. If the U.S. defaults on some of its bonds, lenders may be unwilling to accept those tainted securities as collateral.

Worse, Wall Street’s trading systems have not been set up to separate defaulted Treasuries from the rest. Because few thought a U.S. default was ever possible. This could lead to the short-term lending market grinding to a halt. Similar to the beginning of the global financial crisis.

Global jitters and the impact on investing

An estimate from Moody’s Analytics predicted that the U.S. would slide into recession in a prolonged default scenario. The Gross Domestic Product would fall by almost 4%, and some six million jobs would be lost. The resulting stock market sell-off would erase $15 trillion in household wealth. In the short term, interest rates would spike. In the long term, they would never fall back to pre-default lows.

The worlds anchor asset

Experts say a U.S. default could wreak havoc on global financial markets. The creditworthiness of U.S. treasury securities has long bolstered demand for U.S. dollars. It has the status of the world’s reserve currency. Any hit to confidence in the U.S. economy could cause investors to sell U.S. treasury bonds and thus weaken the dollar.

Securities issued by the U.S. have been treated as essentially risk-free. Dollar denominations underpin a vast number of financial contracts worldwide.

The stability of the dollar has made it the dominant global reserve currency since the end of World War II. This has generated constant global demand for dollars, making it possible for the U.S. government to borrow at lower interest rates than other large nations.

The decrease in the US dollar’s value causes the value of many reserves to drop. This could send ripples through the global treasury markets.

“If it turns out that that asset is not actually risk free, but that it can actually default, that would basically detonate a bomb in the middle of the global financial system. And that will be extremely messy.”

Jacob Kirgegaard, Senior Fellow, Peterson Institute for International Economics

The U.S. dollar is a common currency in much of the world. Some countries have adopted the dollar as the official currency. Often, it exists side-by-side with a local currency that is often “pegged” to the dollar to keep its value stable.

Heavily indebted low-income countries, holding dollar reserves, would struggle to pay interest rates for debt in other currencies. This could result in a debt crisis in emerging markets.

Global trade

Around the globe, many cross-border transactions carry requirements that are settled in U.S. dollars. This is seen as a practical way to be sure that sudden swings in the value of a local currency don’t dramatically disadvantage one party in a transaction that is to be settled in the future.

A sudden and sharp decline in the dollar’s value would mean that individuals and companies anticipating payment on existing contracts in dollars would effectively receive less than they had expected for their goods and services.

In addition, if a default drove the U.S. into recession, U.S. consumers and businesses would reduce the number of goods and services they purchase from outside the country.

While this would impact virtually all countries to some extent, emerging market countries that rely on exports to the United States for much of their income would be particularly hard-hit.

The expected devaluation of the dollar would have a similar impact. It would make it more expensive for U.S. firms to purchase supplies overseas, reducing trade even further.

Capital flow

One of the economic advantages the United States has long enjoyed is that it is a magnet for global capital. When the global economy is strong, invest in U.S. firms. When times are bad, investors seek shelter in U.S. Treasuries. Either way, global markets are directing capital into the U.S.

If investors don’t trust the U.S. government to pay its debts, interest rates go up for the wrong reason. The system will be considered broken.

Thus investors seeking shelter would be more cautious about assuming that Treasury securities are the go-to investment to protect their assets. Investors would begin to direct at least some of their investments to securities issued by other governments and denominated in different currencies.

A new reserve currency

The Dollar instability could benefit the Euro Zone or aspiring power rivals such as China.

For years allies like the European Union and competitors like China have suggested that it would be better if the dollar’s dominance were not as complete as it is.

So far, there has been little movement to unseat the dollar in recent decades. Still, a shock like a default on U.S. debts could persuade some countries to hedge their bets by taking on other currencies, like the Euro or Renminbi, as additions to their reserve holdings.

Personal note by a global investor

We need to stay positive but vigilant. Neither the Republican-led Congress nor the Government would risk such dire consequences – if they really think about it.

The US debt ceiling crisis is a wake-up call for global investors. It highlights the need for vigilance, diversification, and a deep understanding of the interconnectedness of financial markets. By staying informed and adapting strategies, investors can navigate these uncertain times and position themselves for long-term success.

Hopefully, the US parties will find a solution, despite playing the game of chicken now. Frankly, I can not assume that either side really wants to crash the car. In the end, they get there even if delayed and with consequences.

Without a doubt, we will see difficult times; investors must stay vigilant and prepare. Currently, markets still seem undaunted by the prospect of default. But as investors, we need to think long-term. The priority at the moment is to stabilize the portfolio. So, risky and highly leveraged investments might not be the right approach right now -be a bit more defensive.

Speed read

The US debt ceiling crisis rocks global investing, creating uncertainty.

Markets face disruptions, impacting the global economy.

The vulnerability of the US dollar heightens volatility and currency fluctuations. Prepare for potential defaults and downgrades, diversify and manage risks.

Stay vigilant, monitor developments, and adapt.

The interconnectedness of the global financial system needs to be remembered at all times.

Seek opportunities amidst challenges. Stay informed, navigate wisely, and succeed long-term.