WELCOME

Could the Chinese Debt Crisis Affect your Portfolio?

My dear Friends,

Like me, you probably read about the Chinese real estate developer Evergrande and a looming Chinese debt crisis.

Disturbing pictures of people protesting in front of banks or reports of home buyers living in half-finished buildings do not really send a reassuring message in these already difficult times.

You most likely feel for the poor homeowners, but you believe that this could never affect the global economy or your portfolio, for that matter. Really?

Let´s investigate the matter a little further and shine a light on the current Chinese debt crisis.

The Chinese Property Market

China is Asia’s quintessential success story. Since the 1980s, the country has transformed into an economic powerhouse. And Chinese property developers have certainly helped fuel the nation’s rapid economic growth.

Within a few years, its market players owned more assets, in fact, $2,7Trillion, than their North American counterparts, who own assets worth $2Trillion.

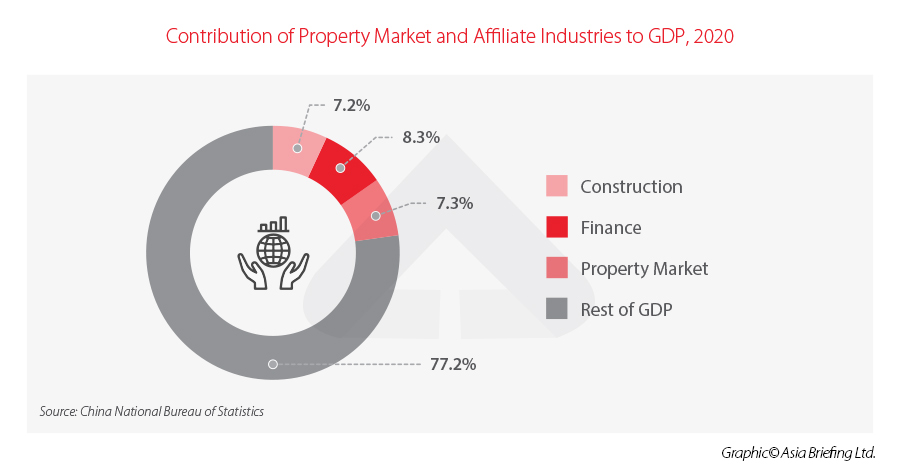

The property market has been a key driver of the Chinese economy since it opened its markets in the 1980s. Today, real estate makes up 30% of China‘s GDP and is a major contributor to the economy.

In 2021, five Chinese property companies ranked among the top ten of the world’s 100 real-estate companies.

However, many experts have warned for years that China’s real estate boom was based on an “unsustainable” model.

Satellite pictures showed developments, some at the size of a city, to be uninhabited. Houses were seemingly built for speculation purposes only. Ghost Cities in the true sense of the word.

Its critics maintained the system only benefited local governments and unnecessarily encouraged people to invest the bulk of their savings in property.

Like every industry that grows too fast, another hazard popped up; too many poor-quality developers flourished as the sector expanded. Structural problems and construction delays are now unfortunately common in this market.

The History

Until 1988, the government owned, controlled and managed all real estate in China. Since then, a market-based real estate industry has gradually developed, related legislation has been enacted, and various types of real estate services have emerged.

During this period, real estate in China changed from a public good to a commercial product.

Over the past two decades, real estate has become an important component of China’s financial markets.

The housing market development can be divided into three stages. The stage of slow release of potential demand driven by the housing reform, 1978–2001. The stage of short supply and soaring housing prices are driven by fast urbanization and industrialization, 2002–2013. Finally, the stage when structural surplus and shortage co-exist, 2014–present.

The market-oriented reform in the first stage paved the way for fast housing market development in the second stage, which in turn laid the foundation for stock optimization in the third stage.

Key Players & StakeHolders

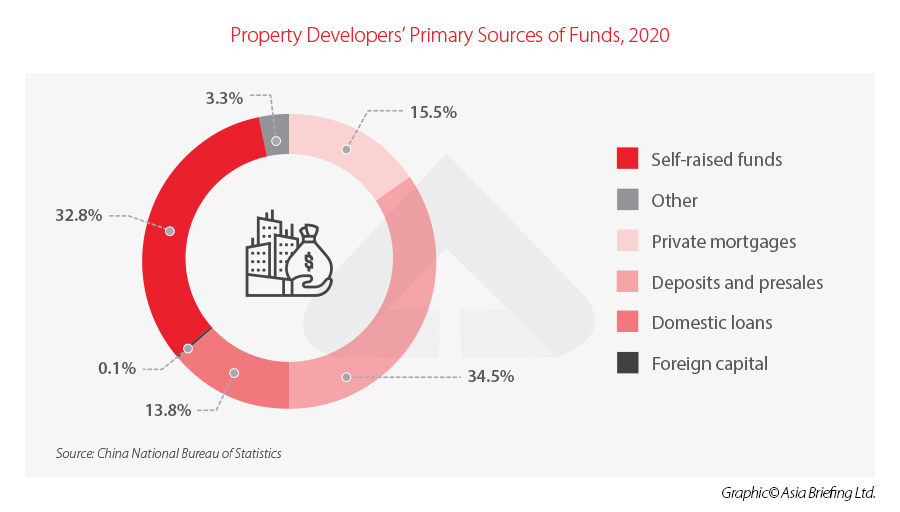

In 2021, about 90% of new properties in China were pre-sold. Up from just 58% in 2005.

These funds are virtually interest-free and are used to pay for construction. But this system has been poorly regulated, and funds are often misused.

The Homeowners

China has one of the world’s largest homeownership rates, reaching 90 per cent in 2020.

For most, the property is seen as a source of economic stability and security. There is a cultural element to this phenomenon. Homeownership is traditionally considered a prerequisite for marriage, particularly for men. For this reason, families and friends will pool money to buy their children property to help them with marriage and family prospects.

Cultural factors aside, it is also clear that buying a home – and even a second or third home – was increasingly considered a savvy financial investment and a well come addition to investors’ portfolios.

This demand has driven home prices up over the last two decades.

A huge proportion of personal assets are tied up in the property sector. As much as 70 per cent of household wealth is in the property.

The Property Developer

Property developers are some of the largest companies in China. They made huge profits off the back of the property boom that China has seen over the past two decades.

According to data from the NBS(National Bureau of Statistics), total commercial housing sales grew from RMB 5.8 trillion (US$914 billion) in 2011 to RMB 17.3 trillion (US$2.7 trillion) in 2020. This is a staggering 21.8 per cent annual growth rate.

Now here is the catch, the largest source of income for property developers were deposits and presales. This indicates a huge reliance on speculative spending from individuals and enterprises.

Another source of liquidity for property developers is credit. In 2020, the property development sector took out a total of RMB 2.6 trillion (US$419 billion) in domestic loans.

These loans have built up over the years. According to the investment bank Nomura, the property development sector had accumulated RMB 33.5 trillion (US$5.2 trillion) in debt as of June 2021.

The Banks

A substantial portion of funding for property developers comes from extensive bank loans. This means that the property market is also inextricably linked to the financial industry. While this is a global phenomenon, it is particularly true in China, where real estate loans accounted for 27.4 per cent of total loans issued in 2020.

Many of the banks exposed to the real estate industry are also some of China’s largest state-owned enterprises, including China Construction Bank, CITIC Bank, and Bank of China.

The Local Government & Financing Vehicles

In China, the government owns the rights to all land in cities. Companies and individuals can purchase land-use rights from the government for up to 70 years, after which the lease can be extended. The property built upon the leased land can be bought and owned by companies and individuals.

In addition, local governments had been prohibited from raising money through bond sales until 2015. For this reason, land sales have been a major lifeline for local governments. It is estimated that revenue from land transfers and real estate special tax together accounted for

Though land sales have helped to fund some of these projects, to sustain the high levels of spending required to drive economic growth, local governments have also had to turn to other sources of liquidity. This is where the use of local government financing vehicles (LGFVs) comes in.

LGFVs are investment companies that are owned by local governments. They were created as means to bypass a ban on direct borrowing by governments. The LGFV can take out loans on behalf of the government to finance infrastructure or welfare projects.

Annus Horribilis

China’s property market plays an outsized role in the global economy. It is intricately linked to core industries, local governments’ performance, investors, and homeowners.

Data from 2021 showed that China’s largest property developers had accrued trillions of dollars in debt. This was cause for alarm among economists and investors alike over fears of financial instability.

The real estate sector had been riding a wave of optimism on the back of record sales in 2020. Yet 2021 turned into an annus horribilis for China’s property market. Some of its largest players defaulted on billions of dollars in debt and plummeting sales numbers – the most prominent, Evergrande.

Though the events that unfolded in 2021 seemingly surprised many industry insiders, they were nonetheless a culmination of long-standing issues, amongst them mounting debt and unsustainable growth strategies.

That volatility was suddenly exposed when a 2020 rule for property developer financing began to stress liquidity.

Trouble in the property sector could cause trouble for China’s economy as a whole. Some analysts are concerned that drops in housing sales and lending curbs will negatively impact economic growth in 2022.

The Crisis

Concerns around China’s property sector sustainability have been circulating for many years. In 2016, the government first felt compelled to use the phrase “houses are for living in, not speculation” to strongly criticise the rise in housing presales and purchases for investment.

“It remains to be seen how the authorities will handle the crisis. They may have postponed dealing with it for too long, because people’s confidence has now been shaken.”

George Soros, Chairman Open Society Foundation

The Redline Policy

In August 2020, the Peoples Bank of China(PBOC) and the Ministry of Housing and Urban-Rural Development held a meeting with other government departments to discuss mechanisms to recognise the risk that the property sector’s debt posed to the economy. They decided to curb borrowing and reduce debt in the property sector. In attendance at the meeting were 12 of China’s largest property developers – who were asked to take action to reduce debt.

Evergrande Saga

The Red Line Policy, designed to curb the boom, made it difficult for indebted real estate giants like Evergrande to pay their debts or raise more capital.

Evergrande is reeling under more than $300 billion of total liabilities, including about $19 billion in offshore bonds held by international asset managers and private banks on behalf of their clients. Evergrande scrambled for months to raise cash to repay lenders.

The company has appealed for more time, but some lenders appear unwilling to wait. Last autumn, the country’s most indebted real estate firm was labelled a defaulter and is undergoing debt restructuring.

At the same time, buyers of an Evergrande project in Jingdezhen, Jiangxi province, fired “the first shot” in the recent repayment protests.

“The Evergrande Longting project in Jingdezhen must fully resume work before October 20, 2022, if not, all the owners who have not paid off their loans will stop repaying the mortgage.”

Buyers, Longting project in Jingdezhen

Analysts have long been concerned that Evergrande’s collapse could trigger wider risks for China’s property market. This could hurt small investors’ real estate portfolios and the broader financial system.

Ripple Effects

China’s real estate crisis is escalating and raising concerns about growing risks in the banking system.

According to multiple state media reports and data compiled by Shanghai-based research firm China Real Estate Information Corporation, buyers across 18 provinces and 47 cities have stopped making payments since the end of June.

The payment boycott comes as a growing number of projects have been delayed or stalled by a cash crunch, like the one that saw giant developer Evergrande default on its debt last year. Several other companies already seek protection from creditors. Home prices are also falling, meaning buyers may be locked into a property that is now worth less than they agreed to pay.

Analysts fear that a payment strike among homebuyers could lead to a vicious circle. As more developers default, putting additional strain on China’s banks.

The Banking System

Although financial institutions usually have real estate as collateral, undelivered projects are worthless. For lenders, the situation is equivalent to bad debts. When bad debts increase, it may cause systemic financial risks.

Since April, four rural banks in China’s central Henan province have frozen millions of dollars worth of deposits, threatening the livelihoods of hundreds of thousands of customers in an economy already battered by draconian Covid lockdowns.

“What concerns us is if more home buyers cease payment, the spreading trend will not only threaten the health of the financial system but also create social issues amid the current economic downturn”

Betty Wang, Senior Economist at ANZ

Citi Financial Services‘ analysts said the boycott could boost bad debts at Chinese banks by $83 billion. This will invariably cause social instability at a time when the country is already grappling with rising protests over the deteriorating health of small, rural banks.

More than 1,000 depositors from across China gathered outside the Zhengzhou branch of the country’s central bank, the People’s Bank of China, to launch their largest protest yet.

China’s economy slowed sharply in March — consumption slumped for the first time in more than a year, while unemployment in 31 major cities surged to a record high.

Several investment banks have slashed their forecasts for China’s full-year growth in the past week. On Tuesday, the International Monetary Fund cut its China growth forecast to 4.4%.

Nasdaq´s Golden Dragon Index, a popular index (EFT) that tracks more than 90 US-listed Chinese companies, lost 31% in the third quarter of 2021, the worst quarter on record. It then shed another 14% in the final quarter of last year.

Editors take Away

I am convinced that the Chinese government will do everything to prevent a total meltdown of the property market. Yet can it avoid a major debt crisis?

Neither can Chinese banks can operate completely disconnected from the international banking system or the international financial markets.

Nor did Chinese real estate companies only borrow money from Chinese people – they issued bonds offshore. Evergrande, for example, issued about $19 billion in offshore bonds held by international asset managers and private banks for their clients.

So yes, there is a real chance that collapsing Chinese banks will affect banks around the globe and the international financial markets.

If this will result in another global financial crisis, like in 2008, remains to be seen. This depends very much on how much “bailing” out the Chinese government is prepared to do.

There is some good news: China’s slowdown could ease global inflationary pressures. A cooler economy could slow consumer spending in China and ease supply chain congestion while keeping the prices of Chinese exports in check.

It remains a fact, however, that a severe recession or social unrest in China is in nobody’s interest.

China is the second biggest economy in the world. A banking crisis or recession there will affect the global economy, one way or another, and, as a consequence, your and my portfolio as well.