Welcome,

10 Questions female investors should ask in difficult times

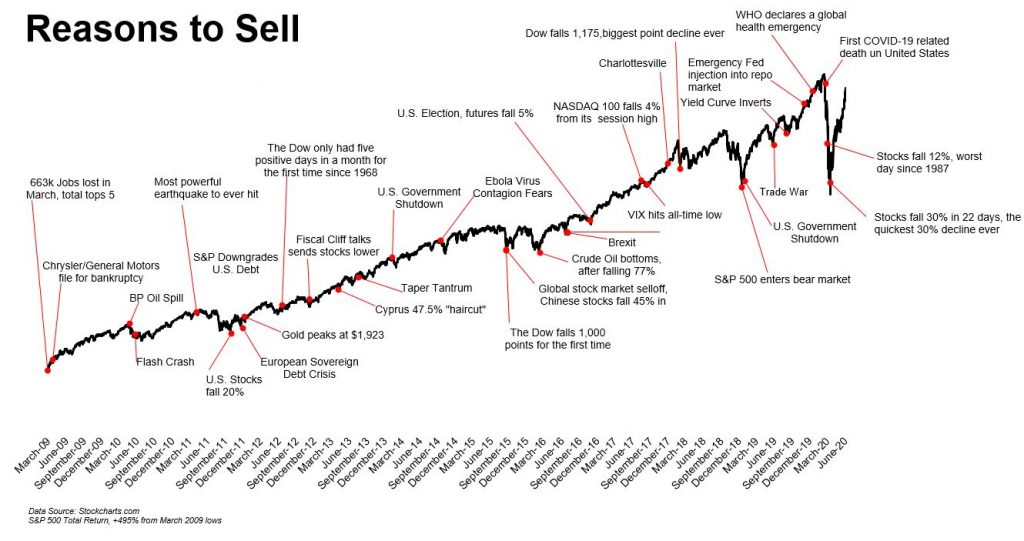

Since the end of 2021, markets turned from bullish to bearish. The war in Ukraine has only accelerated this trend.

My dear Friends,

at the moment, making the right investment choices is not easy. Global economies were still trying to recuperate losses caused by the pandemic when the war in Ukraine turned everything upside down again.

Markets are even more volatile, and energy prices and inflation are on the rise. The only thing we know at the moment is that we have little to no information on what the future will look like.

We neither know the outcome or length of the dispute nor the long-term impact the war will have on the global economy. Will inflation continue to rise? Will interest rates go up? Will commodities become the new gold standard?

We need to stay level headed right now, these 10 questions might help to do that.

Question 1: What is my plan?

Envisage your future and make a written plan. Where do you want to be in 10, 20 or 30 years? What kind of lifestyle do you hope to have? Do you want to leave a legacy? Do you want to build a business?

These plans have financial implications. Such as the extra funding for a business venture or the money you will need to sustain your lifestyle, or the funds you want to assign to philanthropy.

It is paramount to include any liabilities you might be facing, and most importantly be honest with your spending habits.

A plan for your financial future is not about having an idea or following an instinct. Without a plan, you remain in a continuous brainstorming loop and end up bouncing from one short term investment idea to the next. Or, you might end up keeping your money in a savings account. Neither is a very good idea.

Question 2: How much money do I have to invest?

Assess your current financial situation first. This includes your income, any savings, a future inheritance, profits from your business or any other source of funds.

Also, add up any current liabilities like a mortgage, a loan, or any other debt or money owed to someone, like a tax payment.

Don`t sell your house or dip into your emergency fund to allocate money for investments. Neither should you have to sell off family heirlooms to scrape together a large sum of money to start investing.

Question 3: What is my goal?

Saving for a specific item, like a house, is a goal. Building your own business is a goal, as is growing your business.

Maintaining your standard of living in old age or after a divorce is also a goal. So is building an art collection or leaving an impact with philanthropy. Building a perpetual capital pool with a specific purpose is also a goal.

Without answering those questions you will not be able to assess how much risk you are prepared to take, and what sort of duration your investments should be. Neither will you know what sort of future liabilities you are prepared to manage.

Question 4: How much money can I afford to loose?

There’s one golden investment rule that you should always keep in mind: Never invest money that you can’t afford to lose. Nor should you invest the money that you need to meet other responsibilities.

Most investors do not truly know what their stress point of loss is. The most direct way to figure out your true tolerance for loss is … ask yourself.

Every investor has a break point. That is the amount of wealth at which the investment decision making (and maybe their sleeping pattern) is overcome by their concerns about the potential lifestyle impact of their investments.

As an investor, you need to understand, that there is a tradeoff. You can’t talk about how much you are willing to lose without also understanding what that means about how you limit your upside by doing so.

Question 5: How do I manage emotions?

What are you doing about the regular flow of endorphins and adrenaline that course through your veins? How are you managing your fight or flight response? Have you figured out a way to offset the daily onslaught of negative news, brilliant bears and others who might push your emotional hot buttons?

Fear is not what should drive your asset allocations; emotions should be a valid part of your “Buy/Sell” decisions. But it is human nature that these will influence you on a regular basis and at the worst possible times!

Should you have an approach that can not handle these situations well, get a wealth manager to handle the daily decision making for you. This does not mean leaving the decision making to him/her entirely.

Question 6: How can I balance risk and returns with my investments?

Understanding your risk tolerance is key; if you are a conservative investor who takes on too much risk, you may end up panicking and selling your shares at the wrong time.

The potential for greater returns comes with greater risk. Understanding this crucial trade-off between risk and reward can help you separate legitimate opportunities from unlawful schemes.

Investments with greater risk may offer higher potential returns, but they may expose you to greater investment losses. Keep in mind every investment carries some degree of risk and no legitimate investment offers the best of both worlds.

Many investment frauds are pitched as high return opportunities with little or no risk. Ignore so-called opportunities.

Ensure your investing strategy balances risk with the potential portfolio growth needed to sustain your financial future. Talk with a financial professional to determine the appropriate amount of risk based on your age, comfort level, and how much income you’ll likely need. Together, you can develop a clear set of short- and long-term goals that will help clarify your approach.

Question 7: Am I diversified?

Most people should have diversified investments. For example, buying 10 different high-technology companies does not constitute diversification. It is unwise to have investments that will likely drop at the same time.

When you diversify your portfolio, you incorporate a variety of different asset types into your portfolio. Diversification can help reduce your portfolio’s risk so that one asset or asset class’s performance doesn’t affect your entire portfolio.

There are two ways to diversify your portfolio: across asset classes and within asset classes. When you diversify across asset classes, you spread your investments across multiple types of assets. For example, rather than investing in only stocks, you might also invest in bonds, real estate, and more.

When you diversify within an asset class, you spread your investments across many investments within a certain type of asset. For example, rather than buying stock in a single company, you would buy stock from many companies of many different sizes and sectors.

Question 8: How do I know when I am wrong?

Regardless of your positions, what is your objective measure that informs you that something a decision was in error?

You will need a sort of metric that easily determines if a position or allocation or even a belief is in error, so can you course correct.

Most of us hate to admit errors. Everybody is wrong at times, refusing to acknowledge that lacks humility. Being wrong presents a wonderful opportunity for learning, growth and improvement. Don’t ignore your errors but embrace them and make the necessary changes.

There is a golden rule: “Never invest in something you don’t understand”. If you can’t understand the investment and how it will help you make money. Talk to your wealth manager, seek clarification and discuss the investment with him. If you are still confused, you should think twice about investing.

Question 9: Am I prepared to make changes?

If what you are doing is not working, then doing the same thing over and over again won’t fix anything. How much of what you believe has been proven false and must be discarded?

What are you watching/reading/listening to that is counter-productive? What steps have you failed to undertake that are pressing and must be addressed? What are you willing to do to make repairs?

Change is never easy and is especially difficult when money — and ego — are involved. But when in a situation that is not (or has not) been working, it is the only way to improve your results.

Question 10: Should I be managing my own investments?

It is very difficult for a typical investor to beat highly paid, full-time investment professionals.

Much depends on your financial literacy and your financial confidence but, most importantly, it depends on your net worth.

If you fit into the higher-net-worth category, typically above $500,000 or $1 million, you might consider using a wealth manager. Depending upon your ability with financial management and the complexity of your financial situation.

This however leads to one question. “Are my interests and the interests of my investment advisor aligned?” If the answer to that question is no, find a new investment advisor.

Regardless of who you choose, make sure that the person or organisation has a good track record. It’s your money after all.