First and foremost a very happy 2022 to you. I hope you had a splendid start.

The past year was the third year of uninterrupted growth in many stock markets, with the US market taking the lead.

2021 was also a year of recovery from the hits markets had to endure in 2020.

But, what will happen in 2022? Will the new Covid-19 variant dampen investors appetite or will inflation and supply chain problems continue to be a problem?

Will central banks raise interest rates and economies slow down or will we face stagflation?

Promise, I will share everything(almost)women need to know to be prepared for 2022!

2021–Market Recap

In most markets, stocks hit all-time highs. This was mainly due to extensive stimulus packages and available vaccines. The MSCI world index added more than $10 trillion, or 20%.

Economies were grappling with supply chain shortages and rising inflation. Food and energy prices have risen sharply and turbocharged inflation.

Many small businesses were either struggling or forced to give up and labour markets continue to be wobbly.

Europe

European Banks had their best year over a decade with a 34% gain.

Emerging Markets

Equities in Emerging Markets lost 5% overall, which is especially painful as the world index rose by 20% and Wall Street by 27%. Local bonds did even worse with a 9,7% loss.

China

China has seen $1 trillion wipeouts in its heavyweight tech and property sectors.

Turkey

Turkey exits 2021 with a homemade currency chaos inflation soared to a 19 year high due to the Turkish president´s unorthodox money policy. The annual consumer rate rose to 34%. Prices for necessities rose even faster, reaching 54% respectively 44% in December. Turkish government bonds have been hammered as a result.

Cryptocurrency

Bitcoin and other cryptocurrencies had their wildest year yet. Bitcoin´s value hit $70.000 in November, only to drop by 30% in December. By the end of 2021, the entire crypto market had a combined value of $2 trillion.

Mainstream

Owning an NTF has become mainstream. A digital art collage by Beeple sold for $70 Million at Christie’s.

Green has gone mainstream, yet, dirty oil and gas have been the big winners, up about 50% and 48%, respectively.

Commodities

Generally, commodities experienced a surge in demand as resource-hungry economies tried to get back to normal.

The price for corn, sugar and coffee rose by 25%, 22% and 70% respectively.

By the end of 2021, gold took a dive, its worst since 2015. Silver has had its worst year since 2014.

Bonds

Bonds were not a good investment either. Booming inflation and big central banks starting to turn off the money taps have made it a difficult year for bond markets.

Meme Stocks

2021 was the year of meme stocks. Retail investors pushed stocks via social media platforms and got a hedge fund into serious trouble.

Within hours GameStock or AMC Entertainment shares gained 2,500% and 3200% respectively.

Looking into the crystal ball

For 2022 experts predict a bumpy ride for the financial markets. Soaring inflationary pressure, rising interest rates and ongoing disruption to international supply chains caused by the Omicron variant are to blame.

Analysts and financial investors claim that Omicron’s emergence will result in weaker levels of economic growth and intensifying price pressures in already stretched supply chains.

“Our view is that 2022 will be the year of a full global recovery, an end of the global pandemic and a return to normal conditions we had prior to the COVID-19 outbreak”.

Marko Kolanovic& Huissein Malik, Chief Global Market Strategist, Heads of Research, J.P.Morgan, USA

If the pandemic does lose its grip over our lives, central banks are expected to raise interest rates and cut back on their multitrillion-dollar quantitative easing bond-buying stimulus programmes. Mainly to try to rein in inflation.

The US Federal Reserve said this month that it anticipated raising borrowing costs three times in 2022, which could spook markets and weaken a recovery that is already expected to slow in 2022.

Growth matters

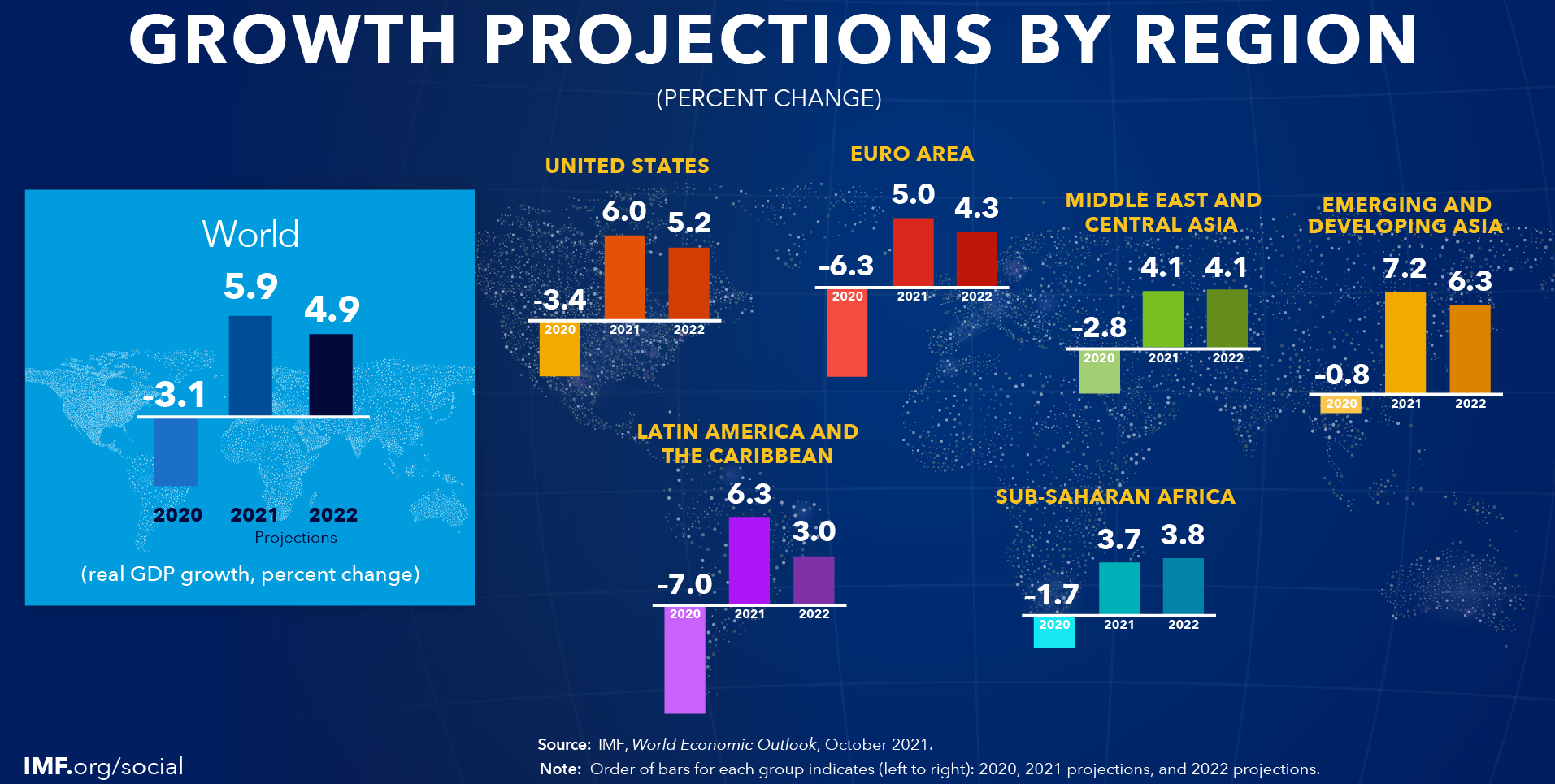

According to the World Bank’s latest Global Economic Prospects report, economies around the world are entering a pronounced slowdown amid fresh threats from COVID-19 variants and a rise in inflation, debt, and income inequality that could endanger the recovery in emerging and developing economies. Global growth is expected to decelerate markedly from 5.5 per cent in 2021 to 4.1 per cent in 2022 and 3.2 per cent in 2023 as demand dissipates and as fiscal and monetary support is unwound across the world.

“Global economic growth is likely to remain above trend for the first half of 2022, monetary policy is still accommodative, even if emergency support measures are being scaled back, and we expect 10% growth in global corporate earnings in the year ahead,”

Mark Haefele, CFO, UBS, Switzerland

The International Monetary Fund(IMF) will release its World Economic Outlook on January 25, a week later than planned. The IMF needs this extra time to factor in any new Covid-19 developments. A downgrade from previous growth projections can be expected.

Hot and fast markets

Research Experts foresee a continuing upward trajectory for the financial markets, despite various Central Banks pondering about raising interest rates.

However, the easy returns, dominated by Tech Titles, belong to the past.

“The US Fed is in the unenviable position of choosing between “persistently high inflation numbers, and persistently overvalued financial markets”.

Victor Golovtechenko, Online Broker, Think Markets, Australia

With less play-money in investors pockets, retail investors will have to rethink and Meme Stocks will go out of favour.

European and Japanese stocks will be a focus for investors in 2022. Why? Because they are still reasonably priced and backed by strong fundamentals.

It is assumed, Central Banks will stay ” broadly accommodative”. Strategists at Morgan Stanley foresee continued robust earnings for companies with strong fundamentals. The easing of supply chain issues and recovering labour markets will fuel sustainable growth rates.

Tighter conditions

The 2021 market boomed on low-interest rates, government stimulus and a huge rebound in earnings.

To achieve another big year, markets will need to tame new risks, like inflation.

Lacking the same drivers of 2021, the stock market will need different protagonists.

Companies will have to prove to have liquidity and strong fundamentals.

“We expect tighter global financial conditions, in particular from Fed rate hikes and rising US rates to again trigger bouts of volatility in markets.”

Joost Beaumont, Strategist, ABN Amro, Netherlands

2022 starts with the US Federal Reserve (FED)moving toward the first rate hike since 2018 to clamp down inflation. The European Central Bank (ECB), could follow soon.

The other markets

Emerging Markets growth rates will be in an uphill struggle. They could however benefit from rising commodity prices.

Most Emerging Markets will grow in the next two years. But, much will depend on individual countries´ Covid tolerance policies.

By mid-2022 a growth downturn is expected for the Asian Markets. Partly due to a spillover effect from China´s slowing economy. The other reasons are shifts in the global supply chain, an ageing population and high household debts.

“Despite Beijing’s recent shift in policy stance, we expect growth to weaken further in spring 2022 on a worsening property sector, rising costs of the zero-Covid strategy, an export downturn and widespread factory closures before and during the Winter Olympics,” said Nomura, which fears “the worst is yet to come.

Analyst, Nomura Bank, Japan

Analysts predicted the Chinese economy to grow by 2,5%-3,5% in Q4 of 2021. Their factors were weather extremes, lockdown measures, and bottlenecks for energy supply. The actual growth however was at 4% which resulted in a growth total of 8% for 2021.

Economic growth is expected to slow sharply in China to a below-consensus of 2.9% in Q1 2022 and 3.8% in Q2, before Beijing’s pain threshold is triggered. Policy easing around spring 2022 could reverse the slowdown and support a recovery in the second half of the year.

Inflation , deflation or stagflation

In December 2021 the US had the highest inflation rate since 1982, namely 7%. The main drivers: staff shortages, real estate, food, cars and building material.

Energy prices, however, were not the driver as oil prices had come down considerably, but shortages in commodities, consumer goods and staff were.

“High inflation has central banks feeling the heat, but by late 2022 we see a very different backdrop, with stagnation a bigger risk than stagflation,”

Analyst, Nomura Bank, Japan

Europe trailed behind by a margin, with an inflation of 5% by December 2021. High energy costs and a disbalance between supply and demand were the main driving factor.

“It might be a gradual deflation rather than an explosive rupture, but it does look like a question of when, not if.”

Laith Khalaf, AJ Bell, Online Investment Platform, UK

Some analysts predict inflation to fade out once issues caused by the pandemic, like supply chain shortages and the hyper-demand for oil and gas will ease.

Many experts believe that inflation will remain above the desired 2% mark for a long time to come.

Central Banks

Putting aside any hyped horror scenarios, there is no hyperinflation. 1929 is not on our doorstep nor do any of the developed economies suffer from Turkey-stile inflation rates.

The FED

In December 2021, the Fed announced measures to curb money supply and reduce inflation. The Fed plans to raise interest rates 3 times over the course of 2022 and to end their bond-buying program.

The ECB

Mme Lagarde and her team at the ECB are convinced that inflation is only temporary and will come down to 1,8% by 2024. The ECB bond-buying program started in 2015, to ease the burden of highly indebted European member states. To stop the program now seems politically too sensitive.

“Goldilocks conditions are ending and the liquidity tide is receding which will disproportionately harm overvalued asset classes and speculative areas of the market”.

Todd Lowenstein, Union Bank, The Private Bank Branch, USA

There are however rumours that the bond-buying program might be reduced and interest rates could be raised in the course of 2022.

Unorthodox Turkey

Turkey´s President and his cronies at the Turkish Central Bank will most likely stick with their unorthodox way to combat high inflation and continue to lower interest rates.

Japanification

South Korea´s Central Bank might be fuelling a Japanification of the Korean economy: no growth, high inflation and low-interest rates.

Japan, on the other hand, is on the brink of economic reawakening. 2022 will bring Japan economic growth numbers similar to the US, with much cheaper stock market multiples.

What you need to know, to be prepared

The cost of going “green“

Meeting agreed climate targets requires an unprecedented structural transformation of the global economy over the next two or three decades.

The CO2 tax, carbon credits or permits, will lead to a rise in energy prices. This results in higher production and construction costs and will lead to rising consumer prices.

“The three main risks lie in a policy mistake causing financial havoc, a disorderly energy transition seeing a surge in selected commodity prices, and a nasty variant escaping vaccine protection,”

mbnAnalyst, Generaly Investments, Luxemburg

The “greenification” of the global economy will have a substantial effect on inflation and cooperate earnings.

Companies who develop the technology needed to make the economy greener and the world a better and safer place will definitely be on the winning side.

How will the super stars fare?

All-time highs for tech companies like Apple, Meta(Facebook), Microsoft, Tesla or Nvidia were going from one all-time high to the next in 2021. The US S&P 500 had its 66th all-time high in November. However, investors in SPAC stocks and small-to-mid cap tech stocks have fallen as much as 80% below their highs.

Valuation

There is a gap between large technology stocks and smaller tech names. Larger companies make up the majority of the stock market weighting, meaning that they can carry the overall index higher even while many smaller stocks move lower.

Big Tech´s valuations are well above their long-term averages, yet the companies are so big that it becomes increasingly harder to grow fast enough to support a higher valuation. Nobody can predict the future, but it seems as though large-cap technology stocks at elevated valuations could be vulnerable to a correction as interest rates rise over the coming quarters.

“High-growth but low-profitability tech stocks may fare badly in a world of higher inflation and rising interest rates.”

Paul Craig, Quilter Investors, UK

Running too hot

When inflation begins to rise as it has, it could be a signal that the economy is “running too hot,” and central banks could start to raise interest rates to get inflation back under control.

Rising rates can make money harder to come by in the broader economy (it becomes more expensive to borrow) and tend to hurt the valuations of many growth stocks.

“We are potentially witnessing the end of the valuation bubble in emerging startups, hyper-growth and companies wearing tech clothing”

Paul Craig, Quilter Investors, UK

This fear is one likely reason why so many growth stocks in the tech sector have traded lower in recent months.

Opportunity

It could be that the real opportunity is in high-quality tech stocks with smaller market caps, those that investors have been viciously selling across the board in favour of “safe haven” large caps.

About Crypto

Bitcoin has risen nearly 70% since the start of 2021, driving the entire crypto market to a combined $2 trillion in value.

Heightened regulatory scrutiny and intense price fluctuations have dampened bitcoin’s prospects lately.

The US Securities and Exchange Commission greenlighted the launch of ProShares’ Bitcoin Strategy ETF this year, the product tracks bitcoin futures contracts rather than giving investors direct exposure to the cryptocurrency itself.

“If I were an investor now I would think about coming out of bitcoin soon because its price will probably crash next year, bitcoin has no fundamental value and serves as more of a “toy” than an investment.

Carol Alexander, Professor of Finance, Sussex Univerity, UK

Some experts believe bitcoin is due for a sharp decline in the coming months.

Not everyone is convinced the crypto party will end in 2022. “The biggest risk factor, namely national banks´ decisions, have been decided and are likely priced in already,” said Yuya Hasegawa, crypto market analyst at Japanese digital asset exchange Bitbank.