Hi there,

The Value of Activist Investors:

Harper’s Pocket Guide to Activist Investing

My dear Friends,

Shareholder activism is again on an upward trajectory after having shaken off its COVID-19 malaise.

Many think activism belongs to the environmental or social issue segment to achieve change for the greater good of society. Sorry to disappoint, but there might be the odd activist investor around with the greater good of society in mind. However, the majority are activist investors to bring value for themselves.

However, if we like it or not, activist investors are here to stay and are radically changing the business landscape.

I hope you are ready to crack the secrets of activist investing and discover a world of value creation! I, Harper, put together an easy-read pocket guide for you so you’ll gain insights into the strategies, techniques, and success stories that have reshaped the investment landscape.

So, hold on to your usual curiosity and let’s take a deep dive into invaluable knowledge together.

– yours, Harper-

Who exactly are they?

Activist investors are shareholders at publicly traded companies who attempt to affect change in an organization. By either directly appealing to or putting heavy pressure on the company’s board of directors. Bypassing the normal advisory process.

Activist investing is a form of value investing, albeit an aggressive one. While traditional or passive value investors believe the share price of an undervalued company will naturally and gradually increase to reflect the company’s true worth, activist investors are determined to increase an undervalued company’s worth more quickly.

The firms that activists target tend to underperform relative to their industry. Due to activists’ aggressive attitude toward management and focus on short-term profit-making, they are often perceived as “corporate raiders,” “green mailers” or “asset strippers”.

Activist investors try to convince other shareholders and the media to buy into their agenda. However, at the end of the day, they are looking out primarily for their own best interests.

Typology

Hedge fund activism is among the most aggressive and involves shareholders. They usually seek a significant change in a company’s strategy, financial structure, management or board composition.

The more conscious activist investor brings value by targeting governance and policies; executive compensation plans; audit and risk management; overall company strategy. The activist investors might also aim at shifting the focus back to core business activities by breaking up or merging large groups.

More recently, activists have been targeting management composition and capital allocation decisions. Activist investors attempt to bring in new management teams, create operational efficiencies, and impose financial restructuring or divestments through the selling off of assets.

The activist´s strategy

Activist investors see weaknesses, flaws or problems resulting in undervaluations. Yet, they also envision solutions in the form of strategic initiatives that they believe will increase shareholder value. The specific initiatives proposed by activist investors can be divided into these four categories.

- Activist investors commonly propose operational cost reductions and strategies to increase revenue.

- An activist investor may demand that a company sell an underperforming division or split the company into several separate business units.

- Activist investors may pressure companies to repurchase shares or pursue other strategies that significantly change the company’s capital structure.

- Activist investors may insist on various changes to the size and composition of the company’s board of directors.

- Campaigns are closing fast and are supposed to hand activists high wins

- Activist investors take a short-term view- long-term company objectives are not on their agenda.

Hostile attackers

Many companies consider activist investors as hostile attackers. Consulting businesses developed a thriving business by compiling plenty of advice on how to fend off the “attacker.” Like creating a special team to deal with activism or building close shareholder relations. Advice focuses on forestalling an attack by regularly reviewing the business portfolio and strategy, ESG issues and strategy, and the company´s governance and executive compensation.

Substantial analytical skills

Activist investors typically have professional analytical skills and substantial business expertise. They use these qualifications to identify companies with untapped value and develop and deliver specific strategy recommendations to capture that value.

An activist investor’s recommendations can range from strategic initiatives, such as restructuring the company, to changing the composition of the board of directors. An activist investor might demand a personal seat on a company’s board or insist on the appointment of certain independent directors. The activist investor may even target specific directors for removal.

The classic playbook

- They buy a large number of outstanding shares of the target company over a short period of time.

- Activist investors directly engage with the boards of directors to argue for their proposed changes. Simultaneously, they publicly propose a specific set of changes for the company by using multiple media channels to gain broad shareholder support.

- Publicity and shareholder support strengthen the negotiating position of an activist investor, although a company may still strenuously resist the activist investor’s demands. Publicity gives the activist investor better negotiating power with the board of directors.

- Stalled negotiations between the activist investor and the company typically escalate into a proxy fight for control of the company’s board of directors. The activist investor pursues additional measures as necessary to effect the desired changes. An activist investor who successfully collaborates with other shareholders to win control of the board then has enough influence to ensure that his or her desired changes are made.

- Sell all shares once the specific objectives are achieved.

” Activist Campaigns are all too likely to destroy value, so it is essential that companies preempt them.”

Boston Consulting Group

The new set of activist investors

A new set of activists has emerged, emphasizing climate and other environmental, employee/human capital, social and governance (EESG-ESG with emphasis on employees) considerations. The activism landscape has also evolved to include dual-purpose activists who combine both TSR(Total Shareholder Return) and EESG arguments and “pincer attacks” from EESG and TSR activists acting independently or in concert against the same company.

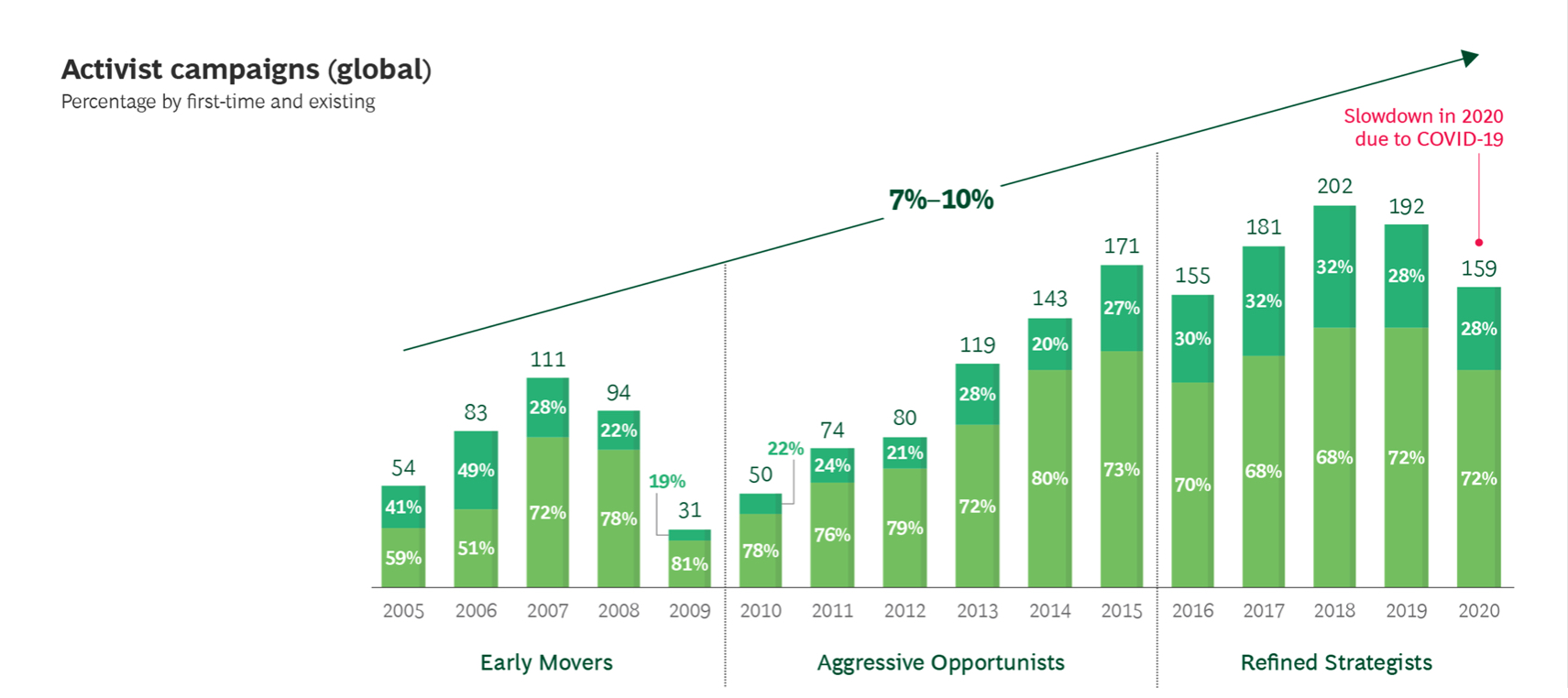

Unlike the “greenmail” campaigns of the past, today’s agendas are often coloured by environmental, social, and governance concerns—a very different shade of green. They are also more successful, with activists winning twice the number of board seats in the past decade than in the one prior.

General theme

However, a Boston Consulting Study observes several cross-cutting themes despite regional distinctions. Where short-term financial engineering may have predominated in the past, activist investors bring value by increasingly pushing for changes that put companies on a stronger long-term footing. More than half of all campaigns globally in the years 2016 through 2020 (55%) were sparked by governance and strategic factors. ESG issues have galvanized particular investor attention, comprising nearly 20% of all activist interventions over the last five years, including climate, diversity, and related demands. The combined assets under management for ESG-driven campaigns now total more than $90 billion, up from $20 billion just five years ago, and these campaigns have become three times more successful over that time.

Take -Away

Shareholder activism is again on an upward trajectory

Activist investing is a form of value investing, albeit an aggressive one

Activist investors see weaknesses, flaws or problems resulting in undervaluations and envision solutions

They buy a large number of outstanding shares of the target company over a short period of time

An activist investor’s recommendations can range from strategic initiatives, such as restructuring the company

ESG issues have galvanized particular investor attention, comprising nearly 20% of all activist interventions over the last five years

The new/old playbook methods include proposing a precatory proxy resolution for actions prescribed by the activist

Four out of every ten campaigns over the past five years occurred outside the US, with the biggest surges in Europe and Asia

Activist Investors try to convince other shareholders to buy into their agenda

Many perceive activists as being smarter than the average investor, but no, they aren’t always right

The activist investor may have a very different investment horizon from the average investor

A changes playbook, really?

Activist investors, including the modern type, are considered an ” attack” on any company. The prevention of, or response to, an activist attack ” is an art, not a science” (Harvard Law School).

Snapshot of the new-old tactics

- Aggressively criticizing a company’s governance, management, business and strategy, sustainability and ESG strategies, and presenting the activist’s own recommendations and business and ESG plan through a “white paper” or other public documents or statements.

- Communicating with and rallying institutional investors and sell-side research analysts to support the activist’s arguments

- Using stock loans, options, derivatives and other devices to accumulate positions secretly, announce surprisingly large, leveraged economic stakes, or increase voting power beyond the activist’s economic equity investment.

- Investing in significant diligence and third-party consulting services to analyze the target’s strategy, business, operating margins and/or ESG impact.

- Reaching a company’s retail shareholders through Internet forums and social media channels, weekly mailings, telephonic outreach, local newspaper advertisements and user-friendly infographics.

- Waging repeated campaigns at the same company, regardless of the outcome of the initial campaign, or joining with other activists to converge on the same company at the same time

Aligning these tactics with ESG standards is difficult. None of the above can be considered good governance.

The good and the bad

Danone

Danone´s C.E.O. had to step down under pressure from the activist investor “Artisan Partners”. Last year, Danone, which owns Evian and several yoghurt brands, was the first public company to adopt the French legal framework of “Entreprise à Mission,” which allows companies to take greater consideration of social and environmental issues in their business model. Ninety-nine per cent of shareholders backed the move, except for “Artisan Partners”. Danone´s performance recently lagged behind its competitors, and “Artisan Partners” demanded a boardroom change and called for an independent chair at Danone for reasons of good governance. At “Artisanal Partners”, C.E.O and chair are held by the same person……

Disney

The hedge fund billionaire Dan Loeb asks Disney to focus on spending more money on their streaming business than on paying dividends. He believes that Disney can build a streaming business that eventually generates more revenue than cable TV and box-office releases, “but only if the company leans into this opportunity and invests more aggressively,” he wrote. By permanently cutting its dividend — worth about $3 billion a year — the company could more than double its Disney+ content budget of about $1 billion a year. Combined with raising the service’s monthly fee, currently $6 a month, and reducing so-called churn, or subscriber defections, the hedge fund thinks that the “lifetime value” of a Disney+ customer could rise to $500, from $100 today.

Third Point LLC

Dan Loeb again: Activist investor Dan Loeb’s Third Point LLC has taken a $750 million stake (equivalent to ~0.4% stake) and stressed that Shell would benefit from breaking into two stand-alone companies. Regarding Shell as an environmental, social and governance investment is the hyper-green explanation offered by Dan Loeb for his move against one of the fossil-fuel industry’s biggest firms. Third Point, an activist hedge fund run by Mr Loeb, revealed on October 27th that it had taken a stake (thought to be worth $750m) in the Anglo-Dutch oil firm. His aim, Mr Loeb declared, is to unleash trapped shareholder value by forcing the breakup of the energy supermajor. The proposal includes asset break-up and a return of incremental cash to shareholders through buyback & higher dividends. Loeb pressures a major oil company to change its strategic direction, as the company faces pressure to reduce fossil fuel investments and pivot to renewable energy amid concerns regarding climate change. In his letter, Loeb pointed out that the past two years had been challenging for Shell shareholders due to a significant dividend cut and a well-publicized court case that ordered changes to Shell’s business model.

Engine N°1

Engine N°1, a small hitherto unknown hedge fund, successfully waged a battle to install three directors on the board of Exxon with the goal of pushing the energy giant to reduce its carbon footprint. Chris James, the founder of Engine No. 1, argued that Exxon’s management wasn’t making needed changes fast enough. The tiny firm wouldn’t have had a chance were it not for an unusual twist: the support of some of Exxon’s biggest institutional investors. BlackRock, Vanguard and State Street voted against Exxon’s leadership, giving Engine No. 1 powerful support. These huge investment companies rarely side with activists on such issues. The stunning result turned the sleepy world of boardroom elections into front-page news as climate activists declared a major triumph and a blindsided Exxon was left to ponder its defeat.

Icahn & Co

Icahn & Co, founded in 1968 as a securities firm, began taking sizable and sometimes controlling positions in companies. Targets have included RJR Nabisco, Texaco, Western Union, Viacom, Revlon, Time Warner, Yahoo!, Motorola, Apple and eBay. In 2015, he pushed Apple CEO Tim Cook to use the company’s cash pile to increase the size of its share buyback program. Icahn Enterprises a diversified holding company that attempts to unlock shareholder value by influencing management or taking a controlling interest. As of December 2019, Icahn Enterprises held significant positions in Herbalife, Cloudera, and Hertz Global Holdings, among other companies.

Active Ownership Capital

On 1 April 2016, the investment fund Active Ownership Capital (Luxembourg), reported having acquired a 5.05% shareholding in STADA Pharmaceuticals. Active Ownership was capable of launching an ultimately successful campaign against the incumbent management. The CEO cited health reasons for taking an indefinite leave of absence on 5 June 2016. However, Active Ownership sought not so much to mend STADA´s strategy or corporate governance but rather to accomplish a sale of the company. The shareholders meeting was finally held on 26 August 2016 and turned into a showdown between management and the activist fund. Half a year after the shareholders meeting, the executive board of STADA disclosed that it considered overtures from three competing private equity firms.29 After what it described as a “structured bidding process”, the board on 10 April 2017 announced its support of a takeover bid by the private equity investors Bain Capital and Cinven, which had increased its offer from 58 to about 65 Euros at the last minute.

Eliott Management

U.S. activist fund Elliott Management(a privately owned hedge fund) has challenged South Korea’s top two family-run conglomerates, first Samsung and most recently Hyundai Motor, over better corporate governance and returns to shareholders. Elliott Management proposed that Hyundai Motor Company pay out a cash dividend of 21,967 won per ordinary share, which was about seven times higher than the per-share dividend payment planned by Hyundai Motor Company (i.e., 3,000 won). The per-share dividend payment planned by Hyundai Motor Company was approved by the ordinary general meeting of shareholders. A report by the SOC Investment Group states Elliott Management’s activist interventions impaired the stock and bond returns, as well as the operating performance, of its target companies.

Global Activism

Four out of every ten campaigns over the past five years occurred outside the US, with the biggest surges in Europe and Asia. Activism in these regions increased by a CAGR of 43% and 44%, respectively, between 2016 and 2020. Companies in Australia, Argentina, Brazil, Canada, and other parts of the world have also witnessed increased investor sabre-rattling, with campaigns growing by a CAGR of 24% over the same period. By contrast, activity in the US rose by only 3%. Many campaigns retain a local character—which means company defences should also. In Asia, for example, shareholder activists are far more likely to be motivated by balance sheet opportunities than their counterparts in other regions.

Last year, there were 106 activist campaigns in Asia, versus 94 the previous year and just 10 in 2011. Asia’s style of business has long been considered ill-suited to activism. Public criticism from disgruntled investors is still fairly uncommon in the region, as they prefer to exert influence behind closed doors. A sense of respect also dissuades activists from embarrassing other business leaders in public.

“In Asia, as regulators look to protect the interests of minority shareholders, corporate governance has risen up the agenda … activist investors now have more power to push for change in the companies in which they have invested,”

David Hunker, JP Morgan

Activism’s resurgence reflects precrisis trends. Campaigns are more global. Institutional investors are increasingly part of the mix, and they have become more vocal in pushing their agendas.

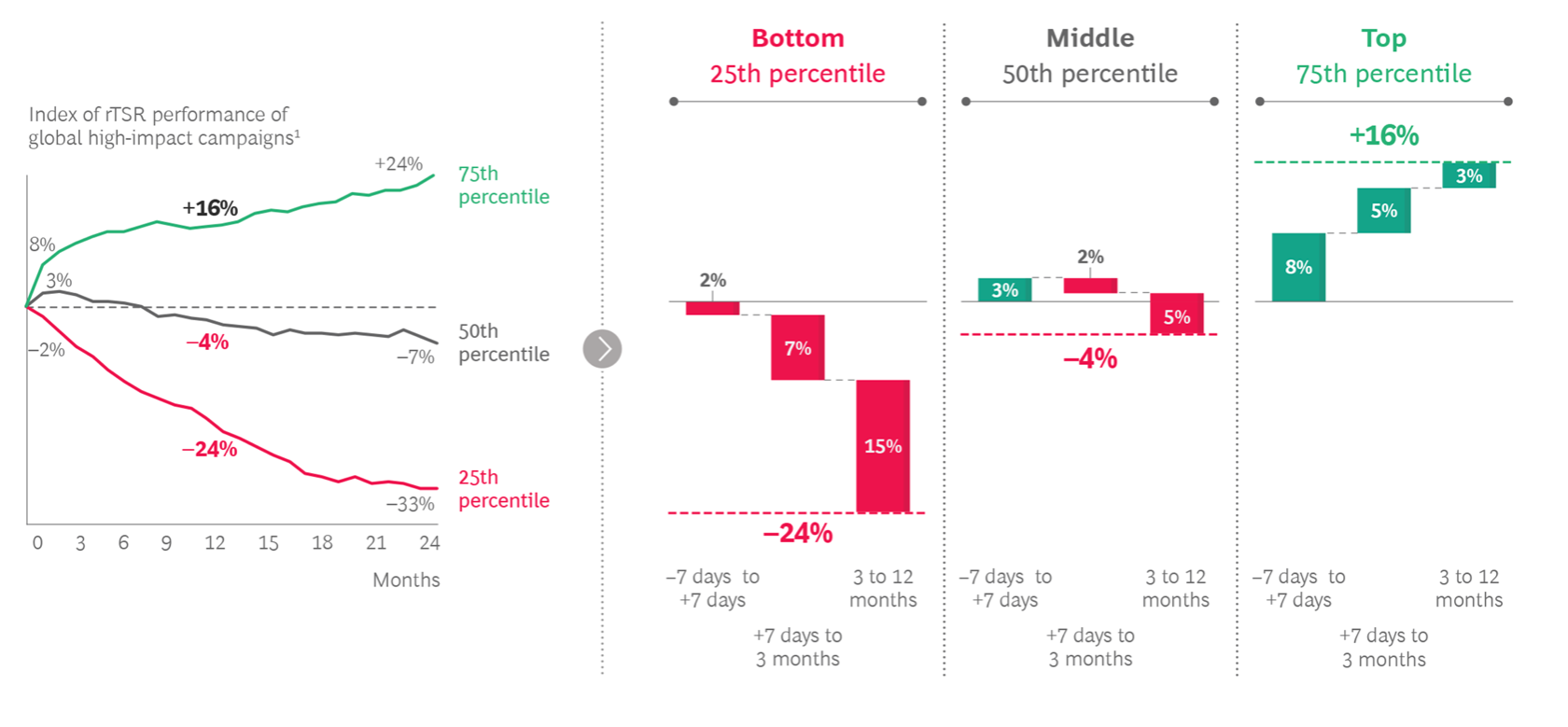

All companies are vulnerable. Although most companies targeted underperformed the market, a fifth, however, had strong shareholder returns. Management can lose control of the narrative quickly, with the TSR trajectory typically determined in the first three months after the attack.

Some activist investors were closely monitoring how companies performed during the pandemic. Not just in terms of financial stewardship, but also in how the company treated its employees and customers during the crisis.

Many activist investors bring value by raising valid concerns. However, many disruption campaigns more often than not destroy value. So it’s essential that companies preempt such actions by adopting a shareholder activist’s mindset.

Do activist investors bring value?

Activists try to convince other shareholders to buy into their agenda, but at the end of the day, they are looking out primarily for their own best interests. It would be wise for investors big and small to keep this possibility in mind when listening to an activist.

On the other hand, the activist investor could be the solution to shareholder passivity. BlackRock recently took a big step by granting voting rights to some of its biggest investors. If this will lead to a shift of power, or force a bold change at BlackRock is doubtful, but a move in the right direction.

“It will allow them to say that they are putting voting power back into the hands of the beneficial asset owners and also deflect some of the criticism that BlackRock has received,”

Douglas Chia, Soundboard Governance

Worth copying?

Many perceive activists as being smarter than the average investor, but no, they aren’t always right. Their timing can be off, and they can and do sometimes lose money. At other times, their good ideas can take an extraordinarily long time to pan out. They can afford to wait it out. Investors should keep this in mind when tempted to copy an activist’s buying or selling action.

While some shareholder campaigns force bold changes that deliver positive near-term results, these are the minority. Most companies lose between 4% and 25% of TSR (total shareholder return) within a year of an activist attack. Senior leaders are also more likely to lose their jobs; data indicate that activism nearly doubles a possible CEO turnover.

Because activists purchase large blocks of stock, smaller investors are usually unprepared when the activist decides it’s time to unload the shares, the share prices drop fast. It’s important to note that activists may have a very different investment horizon from the average investor. And, maybe far more willing and able to accept a loss on their bets.